Part 10: Working Toward a Solution

Part 10: Working Toward a Solution

Billion Dollar Coastline writer Daryl Ferguson sat down with Andy Twisdale (seen here), Chairman of the SC Competitive Alliance, to discuss our state’s homeowners insurance problem and how his organization is working to solve it.

Daryl Ferguson: Andy, you are Chairman of the SC Competitive Alliance. What’s the mission of this non-profit group?

Andy Twisdale: To change the way the SC DOI (Department of Insurance) determines SC property insurance rates so they are more in line with the actual historical incidents of storms; to dispel the myth of hurricane risk in order to encourage fall tourism and encourage more home buyers to consider SC; and to inform property owners and businesses of what mitigation programs and services are available through the SC DOI. Basically, we are a group of seasoned business men and women who want to focus on making the state more competitive. And we also want to solve problems and help give our citizens a better quality of living.

DF: Who is on your board of directors and what’s the background of each of them?

AT: Our committee is comprised of: Stu Rodman, Beaufort County Council; Terry Ennis, retired DuPont executive; Jeff Clacken, retired insurance executive; David Ames, HHI developer; Daniel Riedel, retiree executive from the construction industry; Don McCombs, business executive; Gene Waterfall, retired business owner. These are all business people who have had a career that focused on solving difficult and complex problems.

DF: Why did you become interested in being part of this group?

AT: After reading your research report and the work of Dr. Robert Hunter, of the Consumer Federation of America, it was obvious that SC property owners were paying much higher insurance rates compared with the historical storm-risk data for our state. That bothered me, and I witnessed the problem in my business.

DF: How far has this concern for our high homeowner insurance rates spread throughout the state?

AT: I chaired a state-wide task force for the SC Realtors to look at the issue of property insurance. The task force voted and recommended: the Board of Directors of the 14,000 member organization have adopted legislative action:

1. To rescind the 2004 State law that gives insurance companies an automatic rate increase as long as it does not exceed 7%.

2. To require bi-annual reports to both bodies of the SC Legislature addressing the current status of property insurance rates in SC.

3. To require the SC DOI to hold public hearings throughout SC to receive feedback from property owners on the issues relative to increased rates, increased amount of deductibles, insurance companies requiring more exclusions and customer service complaints.

4. We have made more than 20 presentations to local groups asking for their support. The Charleston Post & Courier and Reporter Tony Bartelme have produced a series of articles called “Storm of Money.” These articles generated by far the most traffic on their website . . .

DF: This past winter the governor’s newly appointed Commissioner of Insurance invited you, Stu Rodman, and me to meet with him to share our concerns. Your presentation was simple yet very impressive. Share with our readers what you presented to Ray Farmer.

AT: Our presentation of the facts by the National Hurricane Center showed that from 1851 – 2009 there were a total of 9 hurricanes, of which one was major. The National hurricane Center projects the number of years for an incidence of a major hurricane to hit Colleton and Beaufort Counties to be 79 years for a Category 3; 210 years for a Category 4; and for a Category 5 . . . 500 years.

There was only one major hurricane in Beaufort County since 1851, whereas the incidence of a major hurricane in Gulfport during the same time frame was nine (9).

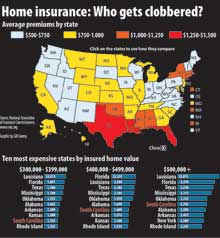

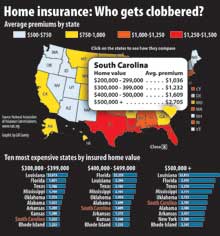

It showed also that in the 5-year period from 2007 – 2011, $33 B was written in direct premiums for property/casualty insurance in SC, yet direct losses incurred during the same time period equaled $18.3 B – a difference of $15 B.

And finally, SC property insurance for homes valued of $400,000 – $499,000 was the 7th highest in the nation.

We thought we made an astounding point: The industry makes an obscene profit from homeowners insurance in SC. Their rates are among the highest in the nation. Yet, our risk for hurricanes is “relatively low.”

Here’s the one point that is most important. We know from our research, and the research of the Charleston Post and Courier, why our coastal hurricane risk is low. In late August, the Canadian mid-latitude jet stream drops down into the U.S. When it does, it soon touches the warm front along our coast. That immediately creates a separate weather system that blows 75% of all hurricanes away from our coast. That fact, and the knowledge that our coastline is concave and 150 miles inland from our natural east coast, is why we know we have a “relatively low risk” for fall hurricanes.

DF: In your opinion how has Mr. Farmer responded to your observations?

AT: At the meeting where we presented these findings, the interim director Ms. McGriff only stated that “I review each rate request to make sure they are correct.” I asked if they had an outside Catastrophe Modeling Company examine these rate increases and there was no response.

As a result of the Senate Banking and Finance appointment hearings which took place over three separate occasions, Mr. Farmer has acknowledged that SC property insurance will be one of his priorities and he will work with our SC Competitive Alliance to address these issues.

DF: Andy, I know that you have personally contacted Mr. Farmer, our new insurance commissioner, and asked him to review certain customer insurance problem cases. Can you give me an example of one or two of these cases where you called Mr. Farmer? What was the problem? Was there any resolution?

AT: Ted Curtis has been a property owner for 10 years on Hilton Head, and has had USAA Insurance Company handling his insurance for 50 years, until 2009. His home is approximately 2000 sq. ft., has a new roof, a 20 ft. elevation, a 2-car attached garage, and he has never made an insurance claim of any kind. In 2009 USAA dropped his Wind and Hail policy and Mr. Curtis was forced to purchase from the SC Wind and Hail Pool with a new rate that was double his previous rate. Present Federal Flood maps show this property is not in the flood zone and HHI has no particular history of hurricane damage. This reputable company, USAA, has willingly underwritten any type of coverage Mr. Curtis has requested for 50 years, but none of that was taken into consideration when they unilaterally dropped the Wind and Hail coverage.

Consumer complaints or concerns to the SC DOI are met with a response that DOI has a Market Assistance Program to solicit other insurance quotes. We also have learned of programs offered by the SC DOI such as a Catastrophic Savings Plan, an Incentive for Mitigation that they offer to consumers, but the response as to “why” consumers have increased rates have not been specific.

One of the most interesting responses was regarding Occidental of NC when a property owner, after the first year of coverage, received a 25% increase. When discussing this with an actuary of DOI, I was told this company came into that marketplace and wrote $7M of premium billings and then decided they weren’t charging enough when they realized what the top 4 companies were charging. I asked “why” they would come into a marketplace not knowing the risk and then, after accumulating $7M in premium billings increase the rates to be more in line with the top 4 companies? It seems to me there was an intentional decision to offer less expensive rates than the top 4 were offering in order to gain a significant number of billings, generate the $7M, and then increase these new customers’ rates by 25% pointing to the top 4 companies as the reason for the increase.

DF: If one of our county or state citizens has a homeowners’ insurance problem that makes no sense, are you willing to review the problem and possibly help the homeowner get a better answer from the Department of Insurance? If ‘yes,’ how would they contact you?

AT: I’d be happy to help. They would need to include the following information:

• The age of the home

• Square footage

• Whether there is an attached or detached garage

• Elevation, if known

• History of insurance rates and any increases

• Whether their homeowners insurance includes Wind & Hail

• Any claims history of the property

• Their email and telephone number

This can be emailed to me at andy@andytwisdale.com

DF: What type of legislation do you believe we need to ensure that the state does not continue as an open door for insurance rate increases?

AT: Regulations that require the DOI to use Catastrophic Modeling Analysis of insurance companies’ rate increases to determine if the increase is justified.

Resend the 2004 SC law that allows for an automatic increase up to 7%.

DF: The insurance lobby recently distributed a “fact sheet” on homeowners’ insurance that your organization challenged. What were two or three of their “facts” that you believe were incorrect? And, in your opinion, what are the correct facts that should have been distributed?

AT: The insurance lobby, R Street, issued:

Policy Study no. 9: February, 2013

Analysis of the South Carolina Coastal Property Insurance Market

This document states: “In the past 10 years SC has seen a negative return on net worth.” Yet, according to the Consumer Federation of America, the return on net worth for SC over the past 10 years has been +22.3% – hardly a negative return.

In this Policy Study there are numerous references to the extent of the SC coastline making it a hurricane-exposed state. However, historically we have had the least amount of hurricane activity on the entire Eastern Seaboard, not to mention the Gulf Coast. In R Street Institute’s own Assessment Risk of Hurricane-Prone States, SC falls into the “Low” assessment risk category, along with Alabama, North Carolina, Virginia and Georgia. Mississippi, Texas and Louisiana are in the “Moderate” category; however, South Carolina’s property owner’s rates are higher than those in “Moderate” states. Therefore, projected risk becomes more important than historical risk, according to the R Street Media.

DF: How optimistic are you that we can make our homeowners’ insurance rates more competitive in the next few years?

AT: I am very optimistic! According to the Consumer Federation of America, insurance companies achieved a return investment of 22% in South Carolina, and the national average by individual states is 5.9%. I feel there is plenty of room for insurance companies to make an industry standard profit and still reduce the cost of property insurance in SC.

But this will only be achieved if SC property owners demand from our state legislators that we want to see a change in the way SC Department of Insurance handles rate increase and its communications to SC residents.

To read more in our Billion Dollar Coastline series, see Local Color

{kind=link}